Picture this: it's a packed Friday dinner service, and a corroded pipe beneath your prep station decides tonight's the night. Water everywhere. Kitchen shutdown. Health inspector on speed dial.

That single plumbing catastrophe — the kind nobody schedules — is precisely why

commercial plumbing insurance cost for small business deserves a front-row seat in your operational budget. Not a footnote. Not an afterthought. A deliberate, studied line item.

This guide cuts through the fog. Real numbers. Real distinctions. And zero tolerance for the kind of vague insurance-speak that leaves you guessing when it matters most.

The Illusion of "Being Covered"

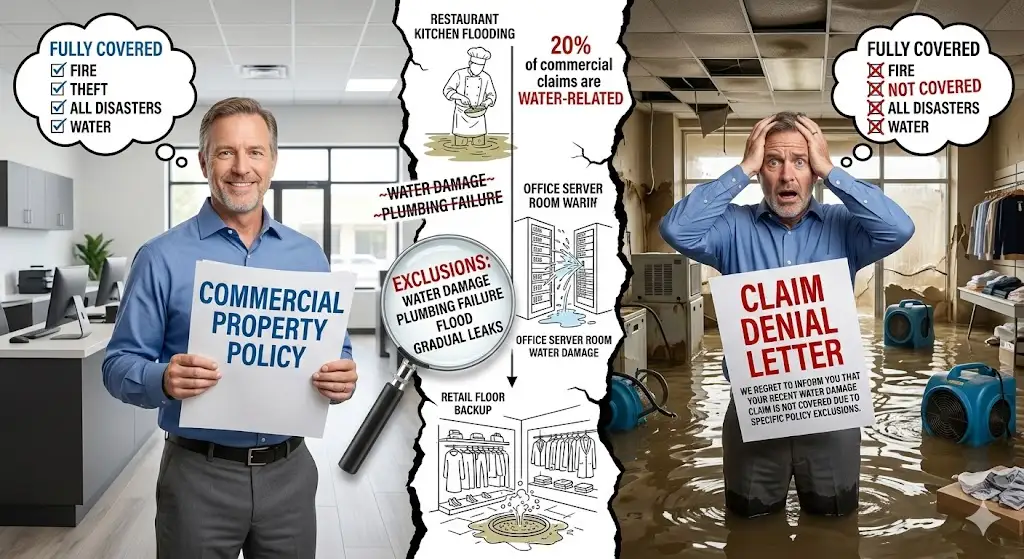

Most small business proprietors operate under a quiet, dangerous assumption: their existing commercial property policy is a catch-all. It isn't. Not even close.

Plumbing-related losses rank among the costliest recurring commercial claims in the country. The Insurance Information Institute has documented water damage and pipe-related freezing incidents as accounting for nearly one-fifth of all commercial property claims filed annually. That's not a fringe risk — that's a statistical near-certainty over the life of your business.

A leaking refrigeration line in a restaurant kitchen. A ruptured supply pipe soaking a law office's server rack. A corroded drain backing up into a boutique retail floor. These aren't hypotheticals. They happen every day. And when they do, the difference between ruin and recovery lives entirely in whether you had the right policy structure in place.

Deconstructing "Commercial Plumbing Insurance"

Here's something the insurance industry doesn't advertise loudly: "commercial plumbing insurance" isn't a discrete product you pluck off a carrier's menu. It's a mosaic of interlocking coverages — each protecting a different vulnerability, each priced against a different risk calculus.

The two foundational pillars:

- General Liability Insurance

- Workers' Compensation Insurance

Conflate them and you'll find yourself holding half a safety net when the floor gives out.

General Liability: Your Shield Against the Outside World

The Scope of Protection

A General Liability Insurance Quote encompasses losses that radiate outward — toward customers, vendors, and third parties whose lives or property your operations touch.

Specifically, it responds to:

- Bodily injury sustained by a non-employee on your premises (a patron who slips on a water-slicked floor from a leaking fixture)

- Third-party property damage (a contracted plumber accidentally ruptures a neighboring tenant's water line)

- Legal defense expenditures when litigation enters the picture

It does not — under any configuration — respond to injuries your own workforce sustains. That distinction belongs to workers' compensation.

What Does It Actually Cost?

General liability premiums for small commercial operations vary considerably, but here's a realistic framework:

| Business Category | Approximate Annual Premium |

|---|---|

| Small restaurant | $800 – $2,500 |

| Office (sub-10 employees) | $500 – $1,200 |

| Retail storefront | $600 – $1,800 |

Your authentic General Liability Insurance Quote will pivot on gross annual revenue, physical footprint, prior claims, geographic risk profile, and the nature of your day-to-day operations. Pull at least three competing quotes before committing.

Worth noting: Any external plumbing contractor you bring onto your property should carry independent liability coverage. If they can't produce a certificate of insurance, their liability migrates — quietly, legally — onto your policy.

Workers' Compensation: Protecting the People Inside Your Operation

The Non-Negotiable Reality

The instant you employ a single wage earner — a line cook, a custodial staffer, a part-time receptionist — most US jurisdictions impose a statutory obligation to carry workers' compensation insurance. This isn't optional territory.

For plumbing-adjacent workplace injuries, this coverage functions as the financial backstop between an injured employee and financial devastation — for both parties. A licensed & bonded plumber employed on your staff (distinct from an independent contractor) is entitled to workers' comp protections covering:

- Falls and slips near moisture-prone zones

- Chemical exposure from industrial drain solutions

- Musculoskeletal injuries from repetitive pipe-fitting work

The Price Architecture

Workers' comp is rated per $100 of payroll, with classifications determining the multiplier. For general maintenance and custodial roles, anticipate a rate of roughly $1.50 – $3.00 per $100 in payroll.

A small restaurant carrying $200,000 in annual payroll could reasonably budget:

$3,000 – $6,000 annually for workers' comp coverage.

Roles involving active plumbing repair command elevated classification rates. Precise job titling in your HR infrastructure isn't bureaucratic tedium — it's a direct lever on your premium.

The Invisible Exposures Most Owners Miss

Business Interruption Insurance

Liability pays for the broken pipe. Workers' comp pays for the injured technician. But neither policy replaces a single dollar of the revenue you hemorrhage while your doors are shuttered for two weeks of restoration work.

Business Interruption Insurance addresses exactly that cavity. It underwrites:

- Net income forfeited during a mandated closure

- Fixed operating overhead — rent, utilities, contracted services — that persists regardless of whether you're open

- Provisional relocation expenses if you must operate from a temporary site

For small businesses, this rider or standalone policy typically adds $500 – $1,500 annually to your coverage stack. Given that a two-week forced closure can erase $30,000 to $60,000 in gross revenue for a mid-volume restaurant, the arithmetic is almost embarrassingly favorable.

Commercial Flood Damage Restoration

This is where coverage gaps become genuinely treacherous. Standard commercial property policies routinely exclude flood damage — sometimes even when the flood originates from an internal plumbing failure rather than a natural weather event. That exclusion language is easy to miss and catastrophically expensive to discover at claim time.

Commercial Flood Damage Restoration coverage — available as a policy endorsement, through FEMA's National Flood Insurance Program, or via private surplus-line carriers — fills that void. Eligible expenditures typically include:

- Industrial water extraction and structural drying

- Mold remediation and air quality remediation

- Structural reconstruction

- Commercial equipment replacement

For any food-service operation, where commercial kitchen infrastructure alone may represent $40,000 – $80,000 in capital equipment, flood coverage isn't a luxury tier. It's a solvency mechanism.

Liability vs. Workers' Comp: The Unambiguous Breakdown

| Exposure Category | General Liability | Workers' Comp |

|---|---|---|

| Customer injury on premises | ✅ | ❌ |

| Employee workplace injury | ❌ | ✅ |

| Damage to third-party property | ✅ | ❌ |

| Injured employee's medical bills | ❌ | ✅ |

| Legal defense costs | ✅ | Limited |

| Lost wages for injured workers | ❌ | ✅ |

The table makes the point plainly: these policies don't overlap. They interlock. Carrying one without the other isn't cost-efficient minimalism — it's structural vulnerability with a premium attached.

Tactical Moves to Reduce Your Premiums

Vet Your Contractors Rigorously

Engaging a licensed & bonded plumber for any commercial plumbing work isn't simply due diligence — it's direct premium protection. An unlicensed tradesperson who causes damage or sustains an injury on your property can redirect those costs squarely onto your policy.

Before any contractor sets foot in your building, collect:

- Active state-issued plumbing license

- General liability certificate (minimum $1M per occurrence)

- Current workers' compensation certificate of insurance

No documentation, no access. That's a defensible policy.

Consolidate Under a Business Owner's Policy

A Business Owner's Policy (BOP) bundles general liability, commercial property coverage, and business interruption protection into a single underwritten package — typically at a meaningful discount versus assembling each policy independently.

For small businesses, annual BOP premiums generally land between $1,200 – $3,500, making it one of the more financially efficient structures available to operations with straightforward risk profiles.

Invest in Preventive Plumbing Maintenance

Underwriters reward documented stewardship. A verifiable maintenance record — annual pipe inspections, grease interceptor cleanings, water heater certifications, backflow preventer tests — does two things simultaneously: it suppresses the likelihood of a claim, and it strengthens your negotiating position at renewal.

Schedule a comprehensive plumbing audit annually. Retain every receipt. Build the paper trail deliberately.

Solicit Competing Quotes — Every Time

Never accept the first General Liability Insurance Quote surfaced by a single carrier or captive agent. Independent brokerage platforms like Insureon and Next Insurance enable parallel comparisons across multiple carriers in a single workflow.

A $400 annual differential, compounded across a decade of operations, represents $4,000 in retained capital. That's not rounding error — that's a piece of equipment, a staff training program, or an emergency reserve fund.

The Variables Underwriters Weight Most Heavily

When carriers price commercial plumbing insurance cost for small business, these factors exert the most gravitational pull on your final number:

- Plumbing system age and infrastructure condition — legacy galvanized or cast-iron systems trigger surcharges

- Annual gross revenue — higher revenue typically necessitates elevated liability limits

- Prior claims history — a single prior water damage claim can inflate renewals by 20–40%

- Geographic risk factors — flood plains, freeze-prone climates, and dense urban building stock amplify exposure

- Business classification — restaurant kitchen plumbing carries measurably higher risk than a professional office suite

- Employee headcount and payroll composition — foundational to workers' comp pricing

Understanding these variables transforms you from a passive premium recipient into an active participant in your own risk economics.

A Practical Annual Budget Framework

For a small US operation — under twenty employees, moderate revenue — here's a realistic annual coverage budget:

| Policy Layer | Estimated Annual Cost |

|---|---|

| General Liability | $500 – $2,500 |

| Workers' Compensation | $1,500 – $6,000 |

| Business Interruption Insurance | $500 – $1,500 |

| Commercial Flood Coverage | $700 – $2,000 |

| Aggregate Range | $3,200 – $12,000 |

Measured against the average commercial water damage claim — which Travelers Insurance places well above $75,000 for mid-size commercial losses — those premiums reframe themselves as the cheapest operational insurance you'll ever buy.

Final Reckoning

Here's what this entire conversation distills to: commercial plumbing insurance cost for small business is not a fixed expense — it's a negotiated, manageable, and deeply consequential investment. General liability guards your perimeter against external claims. Workers' comp protects the people driving your operation. Business interruption coverage sustains your revenue stream through forced dormancy. Flood damage restoration coverage ensures that one catastrophic pipe event doesn't permanently shutter your doors.

Don't let inertia make your coverage decisions. Solicit a General Liability Insurance Quote this week, pressure-test it against a bundled BOP, confirm every plumbing contractor you engage is genuinely licensed and bonded, and build your flood coverage layer before you need it — not after.

Businesses that outlast their disasters don't stumble into resilience. They engineer it, deliberately, one policy at a time.

Thank you for investing your time in reading this through to the finish line — it genuinely means something. If this reshaped how you think about your coverage architecture, I'd love to know. Drop your thoughts, questions, or your own cautionary tales in the comments below. Every perspective sharpens the conversation, and yours is worth hearing. 👇