Inheriting a house sounds like a gift — until you realize you have to share it with siblings who can't agree on anything.

Whether it's the family home where you grew up or an investment property your parents left behind, selling inherited property with multiple heirs is one of the most emotionally charged legal situations you'll ever face. You're grieving, you're stressed, and suddenly you're also navigating capital gains tax, probate court, and a sibling who refuses to budge.

This guide breaks it all down — the tax stuff, the legal stuff, and the human stuff — so you can move forward with clarity instead of chaos.

Why Selling Inherited Property Gets So Complicated

It's not just about money. It rarely is.

When a parent dies, every sibling comes to the table with different memories, different financial needs, and different ideas about what "fair" looks like. One sibling might have lived in the house for years. Another might desperately need the cash. A third might want to keep it in the family forever.

These emotional dynamics collide with cold legal and financial realities — and that collision is exactly where disputes blow up.

The core issue? Multiple heirs means multiple decision-makers. In most states, all co-owners of an inherited property must agree before it can be sold. If even one person objects, the process can stall — sometimes for years.

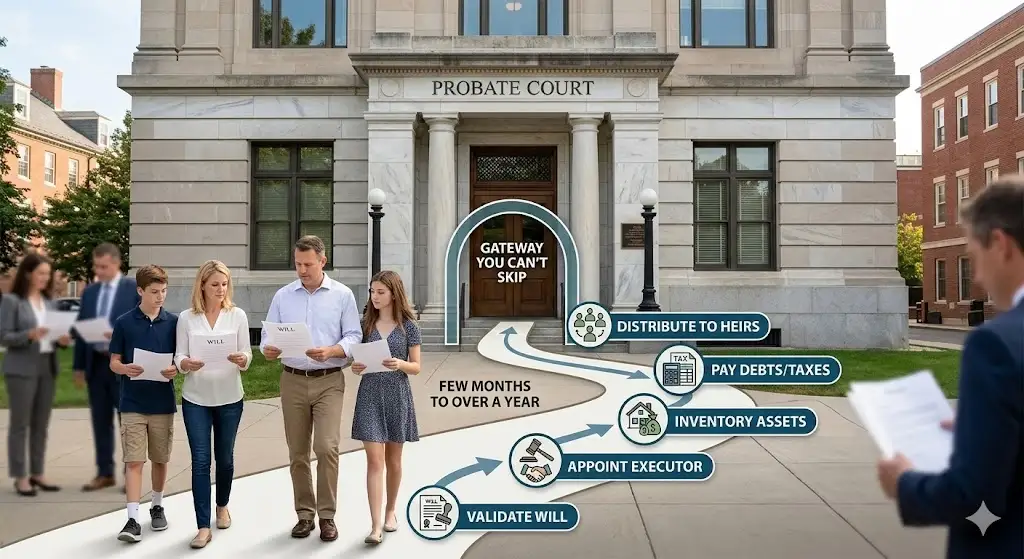

Understanding Probate: The Legal Gateway You Can't Skip

Before anyone can sell anything, the estate typically has to go through probate — the court-supervised process that validates the will and transfers legal ownership to the heirs.

What Probate Actually Involves

- Appointing an executor or administrator

- Inventorying and appraising the estate's assets

- Paying off debts, taxes, and estate expenses

- Distributing what's left to the heirs according to the will (or state law if there's no will)

Probate can take anywhere from a few months to well over a year, depending on the state, the complexity of the estate, and — you guessed it — whether the heirs are fighting.

What Happens If There's No Will?

If your parent died intestate (without a will), state law determines who inherits what. This is called intestate succession, and it typically splits assets equally among children. It sounds fair on paper, but it can create co-ownership situations that are genuinely difficult to unwind.

Working with an estate planning lawyer from the start — even after the fact — can help you understand your rights and options before things escalate.

The Tax Reality: Capital Gains and What You Owe

Here's where a lot of people get blindsided. Inherited property comes with unique tax treatment that's actually more favorable than most people expect — but there are still traps to watch out for.

The Step-Up in Basis: Your Best Friend

When you inherit property, you don't inherit it at the price your parent originally paid. Instead, your cost basis is "stepped up" to the fair market value on the date of death.

Here's why that matters enormously:

Say your parents bought their home in 1985 for $80,000. By the time they passed, it was worth $450,000. If you sell it shortly after inheriting it for $460,000, your taxable gain is only $10,000 — not $380,000.

This step-up in basis is one of the most significant capital gains tax exemptions available in the U.S. tax code, and it applies to inherited property regardless of how long you hold it.

Short-Term vs. Long-Term Capital Gains on Inherited Property

Normally, assets sold within a year are taxed at higher short-term capital gains rates. But inherited property is treated differently — it automatically qualifies for long-term capital gains rates, no matter how quickly you sell after inheriting.

Long-term capital gains rates are 0%, 15%, or 20% depending on your income. For most middle-income earners, that's 15%.

Using an Inheritance Tax Calculator

Before you make any decisions, it's worth running the numbers through an inheritance tax calculator (many are available free online through financial planning sites). Plug in:

- The date-of-death appraised value

- Your expected sale price

- Each heir's share percentage

- Your individual income (to determine your capital gains rate)

This gives every sibling a clearer picture of what they'd actually walk away with — which often moves negotiations forward faster than any family meeting could.

State Taxes: Don't Forget These

A handful of states still levy their own inheritance tax or estate tax separate from federal rules. As of 2025, states like Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania have inheritance taxes. Rates and exemptions vary widely.

If the property is in one of these states, consult a local estate planning lawyer before assuming your federal step-up in basis is the whole story.

What To Do When Siblings Won't Agree

This is the part nobody wants to deal with — but it's often the most important.

Step 1: Get Everyone on the Same Page Financially

Most sibling conflicts aren't really about the house. They're about feeling unheard, or fearing they'll get less than they deserve.

Start by getting a professional appraisal so everyone has the same baseline number. Then share the inheritance tax calculator results so each sibling can see their realistic net proceeds. Concrete numbers often dissolve abstract arguments.

Step 2: Bring In a Probate Real Estate Agent

A probate real estate agent is a specialist — not just a regular Realtor. These agents understand the legal constraints of estate sales, know how to work with executors and attorneys, and are experienced at managing multi-party transactions where everyone has opinions.

They can also help set realistic price expectations, which matters when one sibling thinks the house is worth twice the appraisal because "it has sentimental value."

Step 3: Consider a Buyout

If one sibling wants to keep the property and others want to sell, a buyout might be the cleanest solution. The sibling who wants to keep it pays out the others' shares, typically using a cash-out refinance or a home equity loan.

You'll still need a formal appraisal, and the transaction should be handled by a real estate attorney — not just a handshake — to protect everyone involved.

Step 4: Mediation Before Litigation

If negotiations break down, consider mediation before anyone files a lawsuit. A neutral third-party mediator can often resolve disputes in a matter of hours or days, at a fraction of the cost of going to court.

It's worth the investment. Seriously.

Step 5: Partition Action — The Nuclear Option

If no agreement can be reached, any co-owner can file a partition action in court. A judge can then order the property sold, with proceeds divided among the heirs.

This is expensive, time-consuming, and emotionally brutal. It also tends to result in lower sale prices because partition sales are often handled as forced sales. Consider this the last resort, not the first move.

How to Actually Sell the Property (Once Everyone Agrees)

Okay, so let's say the hard part is behind you and you're ready to sell. Here's the practical path forward.

Get Probate Closed (Or Confirm You Don't Need To)

In some cases — like if the property was held in a living trust — probate isn't required. But in most cases, you'll need the probate court to formally transfer title before you can close on a sale.

Your estate planning lawyer or probate attorney handles this. Don't try to navigate it yourself.

Hire a Probate Real Estate Agent

Yes, this deserves repeating. A probate real estate agent knows how to:

- Price estate properties accurately (they often need work)

- Market to buyers who understand the as-is nature of estate sales

- Coordinate with multiple co-sellers who may be in different states

- Manage the closing paperwork that's unique to probate transactions

Ask specifically about their probate experience. A specialist will serve you far better than a generalist here.

Decide on Sale Format

You have options:

- Traditional listing on the MLS for maximum exposure and price

- Cash buyer / investor sale for speed (typically 10-30% below market)

- Estate auction which can work well for unique or high-value properties

The right choice depends on your timeline, the property's condition, and how quickly the heirs need their money.

Split Proceeds According to the Estate's Terms

Once the sale closes, the escrow company or attorney distributes proceeds to each heir according to their share. Make sure everyone reviews the settlement statement before closing — not after.

Common Mistakes That Cost Families Thousands

Avoid these if you can:

- Waiting too long to sell — carrying costs (mortgage, taxes, insurance, maintenance) eat into proceeds every month the property sits

- Skipping the appraisal — underpricing or overpricing both hurt you

- Not accounting for capital gains — especially if the property has appreciated significantly since the date of death

- Ignoring state-specific inheritance taxes — what applies federally doesn't always apply locally

- Letting emotions drive decisions — the house is an asset now; treat it like one

Quick Reference: Key Terms to Know

| Term | What It Means |

|---|---|

| Probate | Court process to validate a will and transfer assets |

| Step-Up in Basis | Inherited property's value resets to date-of-death value for tax purposes |

| Partition Action | Court-ordered sale when heirs can't agree |

| Estate Planning Lawyer | Attorney specializing in wills, trusts, and estate administration |

| Probate Real Estate Agent | Realtor trained to handle estate and probate sales |

| Capital Gains Tax Exemption | The tax benefit from the stepped-up basis on inherited property |

Wrapping Up

Selling inherited property with siblings is one of those situations where the emotional weight and the legal complexity collide in the most inconvenient way possible. But it's manageable — especially if you go in with the right team and the right information.

Start with a clear appraisal, use an inheritance tax calculator to get everyone on the same financial page, and bring in professionals who specialize in this space: a probate attorney and a probate real estate agent who've navigated these waters before.

The long-tail reality of selling inherited property with multiple heirs, taxes, and capital gains is that the tax treatment is often more favorable than people expect — and most family conflicts can be resolved without a courtroom, as long as someone steps up to lead the process calmly and fairly.

You don't have to let grief and conflict define this experience. With the right support, you can close this chapter in a way that feels fair to everyone — and maybe even keeps the family intact.

Thanks for reading all the way through. If you've been through this yourself or you're in the middle of it right now, drop a comment below — your experience might be exactly what someone else needs to hear. And if something wasn't clear or you'd like me to go deeper on any piece of this, let me know. I'm here for it.